WARNING. THIS ESSAY IS NOT YET READY FOR READING. I HAVE PUBLISHED IT FOR THE PURPOSES OF SHOWING A FRIEND. FEEL FREE TO READ IT IF YOU LIKE, BUT PARTS OF IT WILL BE GIBBERISH. I PROMISE THE REAL VERSION WILL BE DONE FAIRLY SOON.

On the urging of @Sufjansimone I’ve been spending some time lately thinking about inflation. It’s a seemingly boring topic, but I can’t help but feel that it has hidden political and even ethical dimensions that can be unpacked. As far as I can tell, no one has yet written on the philosophical dimensions of inflation measurement, although the intricacies of inflation measurement have long been debated by economists under the aegis of the Index Number Problem. Nothing I’m going to argue here is very novel, indeed I think it’s all pretty obvious once it has been pointed out. Yet I’m hoping it might be a curative draught against the (for want of a better term) reification of certain types of economic variables.

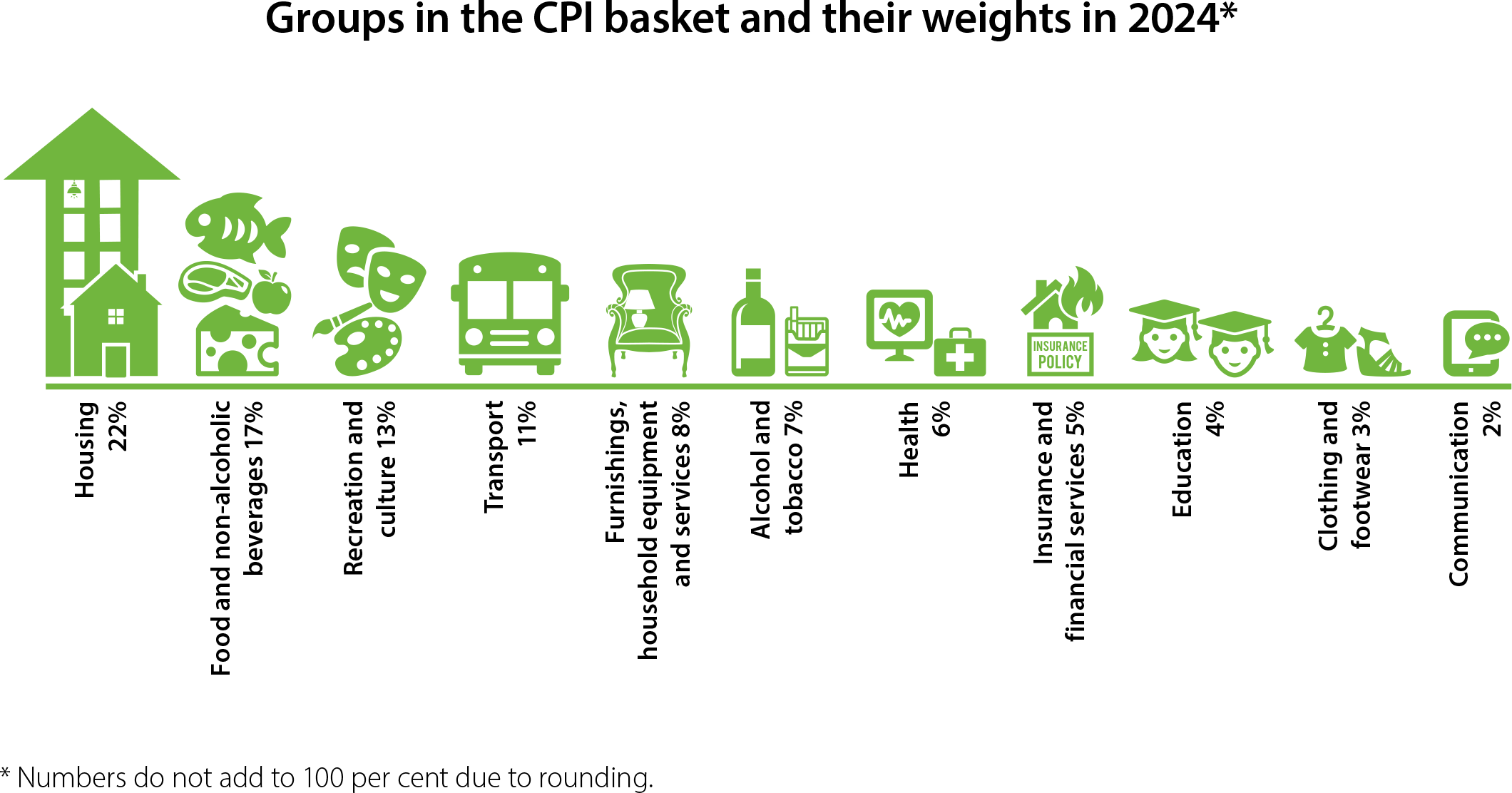

How inflation is normally calculated: A guide for the perplexed

XXX

Thinking about the difficulties inherent in calculating inflation

The value of money at a given time is not a single number- it’s a vector with each dimension of the vector representing the price of a different good. The value of money at a second time is another vector. The dimensions of this second vector might be very different- products enter the market and leave the market due to changes in taste, technology and other factors. It’s not even clear how many products there are which can be purchased at a given time- for example, is a New York big Mac a different product to a Cheyenne big mac? No? Then how come they cost different amounts?

When considering money over time, we try to reduce the enormous complexity inherent in comparing what money can buy at time 1 against what it can by at time 2 to a single scalar- a percentage representing how much prices have risen or fallen- inflation.

It’s not at all clear to me that there is a right or wrong answer when it comes to inflation. Existing measures are roughly trying to capture a representative sense of the changing value of money on a household- but the construction of those indices are a little vague and ad hoc. Is there some perfect platonic number of “true” inflation that these indicies are trying to capture? If so, what is it. Even if we could construct a non-arbitrary definition of the “true” inflation rate, is it likely that there would only be one? Consider how many sensible and non-arbitrary definitions there are of what the center of a triangle is- dozens at the very least. Yet it is hard to single one of these out as the one “correct” definition. https://en.wikipedia.org/wiki/Triangle_center

The role of scientfic and ethical values in comparing the value of money at two times

The first thesis I want to argue for is that in deciding how we are going to go about calculating the value of inflation we need to consider the purposes to which the statistic will be used. Hence it may be wise to have multiple inflation figures, representing different methodologies of calculation for different purposes. We should be pluralists about inflation.

The second thesis I want to argue for is that at least some of those figures should explicitly be worked out with reference to our political and ethical values- e.g., making sure that we are tracking the situation of the vulnerable, and that they are not being crushed by changes in the value of money. Furthermore, we should explicitly argue that these inflation figures- built on the basis of a concern for human welfare- are by no means “supplementary” or in any way of secondary importance. Macroeconomic policy should ideally take these value-informed inflation figures very seriously.

Hedonic pricing

XXX

Positional goods and inflation under hedonic pricing and the problem of circularity

An aside. Economic sociologist Thorstein Veblen argued that part of the value of many goods was their potential for conspicuous consumption. That is, being purchased and used as a display of wealth. Modern research has tended to support the important of positionality in both consumption and income. Much of the apparent extra value of new goods is probably not due to technological advantages etc. but the fact that the latest product confers a positional advantage on its buyer- marking them out from the crowd.

This potentially creates a distorted view of how much quality is increasing- it seems like the new model must be a lot better because people are willing to pay so much more for it- but actually this is just because they just wanted to have the newest and therefore showiest model.

This also has the potential to create an interesting circularity. How much the product is worth partly depends on how much it costs, but when calculating inflation figures using hedonic regression we are partly trying to work out how much it costs (in real terms) based on how much it’s worth. Of course as Kieran has pointed out to me we can tease apart the degree of positionality of a good from its other properties, but it’s still a fun conceptual problem to think about.

Some interesting inflation measures

I think it’s interesting to explore what happens if we treat people not as trying to purchase goods, but instead as trying to purchase lifestyles. For example, a lifestyle of financial satisfaction, or a lifestyle of economic security (in the sense of being able to reliably afford essentials) or a “decent standard of living” in whatever sense that is normally meant by the public.

On that basis, it’s worth imagining some alternatives to official inflation indexes.

Cost-of-Satisfaction inflation index

There are numerous surveys of financial satisfaction. For example, one can ask a person “on a scale from 0 to 10, how satisfied are you with your financial situation?” We could pick some level of satisfaction as a minimally satisfactory level e.g. 7/10. We could then look at what is the lowest level of income that is associated with at least a mean financial satisfaction level of 7/10 is. We could call this the cost-of-satisfaction inflation index.

Decent standard of life inflation index

Ask a representative sample of people what they think the minimum income needed to live a “decent” life is. Look at how this number goes up or down over time and call this the Decent standard of life inflation index.

Economic security inflation index

Ask people a series of questions “do you ever worry about having enough money left for rent”. “Do you ever have worry about having enough money left for food”. “Do you ever worry about having enough money left for medical expenses” etc. Find the lowest income level at which a majority answer yes to all questions. Watch how this level changes over time. We could call this the economic security inflation index.

The meaningfulness of macroeconomic variables

One point worth making: GDP, economic growth and similar national accounts figures really only make relative to an accepted level of inflation. John Maynard Keynes explicitly observed these consequences, arguing:

To say that net output to-day is greater, but the price-level lower, than ten years ago or one year ago, is a proposition of a similar character to the statement that Queen Victoria was a better queen but not a happier woman than Queen Elizabeth — a proposition not without meaning and not without interest, but unsuitable as material for the differential calculus. Our precision will be a mock precision if we try to use such partly vague and non-quantitative concepts as the basis of a quantitative analysis.

How can we deal with this challenge to the meaningfulness of macroeconomic variables outlined? One strategy would be to make sure that we are very confident of our definition of inflation- that it really tracks the things we most care about, re: price changes- that it is optimized to connect with other variables that matter according to our best theories etc.

This will get us up to a certain point, but it’s hard to see how a definition could be perfect, so another problem of diverging definitions of inflation might be sensitivity analysis. We simply see whether, in practice, different plausible operationalisations of inflation converge on the same outcomes.

Appendix for those with an economics background: How to successfully incorporate values into economic measurements- the case study of inequality measures

When you think about it, there’s no one single obvious way to define inequality. Popular approaches include the range, the Palma ratio and the Gini, Theil & Atkinson indices. In this regard, measures of inequality are a lot like measures of inflation. We might say that what can be definitively said about inequality only amounts to a partial ordering. For example, no one could deny that a society where there are four citizens, and they make 20, 20, 20 and 100 dollars a day respectively is less unequal than a society where there are four citizens and they make 19, 19, 19 and 100 dollars a day respectively. So there are some circumstances in which we can definitively say that inequality is higher or lower here or there. The same is true of inflation. If all prices remain static and no new products enter the market, there is clearly less inflation than if all prices rise by one dollar and no new products enter the market. Yet as with inflation, there are circumstances where the degree of inequality, and even the ordering of how unequal different societies are, will come down to definition. Is a society where the four citizens make respectively 20, 20, 80 and 80 dollars more or less unequal than a society where the four citizens make respectively 25, 25, 60 and 80 dollars? That’s going to depend on the formula you use inequality.

So there are many different definitions of inequality. How do we pick which ones get center stage? I would suggest that there are three criteria:

- Social predictive relevance- A measure of inequality has social relevance to the degree that it can be used to predict outcomes of interest. For example, social unrest, crime etc.

- Ethical relevance- A measure of inequality has ethical relevance insofar as it predicts human welfare. For example, the Atkinson index, if the parameters are set correctly can be used to tell us how “good” an income distribution is from a utilitarian perspective.

- Aesthetic beauty/simplicity- The Gini index “makes sense” insomuch as it visually corresponds to the area under the Lorentz curve. The Hoover index is “the proportion of total income that would need to be redistributed to achieve perfect equality”.

Note that all of these dimensions also potentially apply to inflation indicies .Arguments about which inequality index to use are therefore a lot like I’m suggesting arguments about inflation measures should be seen- contextual to purpose and conducted explicitly in terms of both intellectual and ethical values.

Appendix: A stab at an “objective” definition of “true” inflation

I think the best try I can make at fixing a single unique “true” value of inflation- even though it shall never be observed and so is of only ontological not epistemic significance- is as follows.

Take a person who represents the average of everyone’s tastes (whatever that means) at T2.Now offer them an alternative between X dollars at T1 prices, and Y dollars at T2 prices. When we find two sums that they are indifferent between, then Y/X is equal to the inflation rate.

Excepting a highly unethical use of simulated minds, it is deeply unlikely that we’ll ever be able to observe this directly, but it is cute to think about.

Here’s something arbitrary about the above definition. We could just as easily use the average of everyone’s taste’s at T1 to define the agent’s tastes. Or we could use the average of everyone’s tastes at T1 & T2 (how do we deal with population change here? lol.) Anyway, it’s a mess of nonoperable terms and it still doesn’t work smoothly internally! If there is a true definition of inflation which our particular instruments only approximate, it’s very hard to get at.

I am looking forward to seeing this fleshed out, even though it’s a placeholder. I have spent some background cycles pondering similar questions. One idea is to anchor everything to the total amount of labor required to produce a good.

A Big Mac costs $3.99, but I estimate that it probably costs half an hour’s worth of human labor to produce one, which comes out to $7.98/hr. Much of that cheap labor comes from outsourced manufacturers and farmers. And much of what makes the labor expensive are the executives in charge.

It could then be possible to measure the change in the amount of human labor required to produce a basket of basic goods (food, clothing, shelter) over time.

LikeLike